Your entire financial life.

Computed from first principles.

Every person has two questions about money: Where is it going? and What should I do? This app answers both — with the rigor of a finance PhD/professor, the precision of an engineer, and the obsession of a relentless optimizer.

The founder’s actual numbers. 10 years. Professor’s salary. Five kids. Every penny tracked.

Free financial tools

Powered by a 50-state tax engine. No login. No ads. No data collected. Just answers.

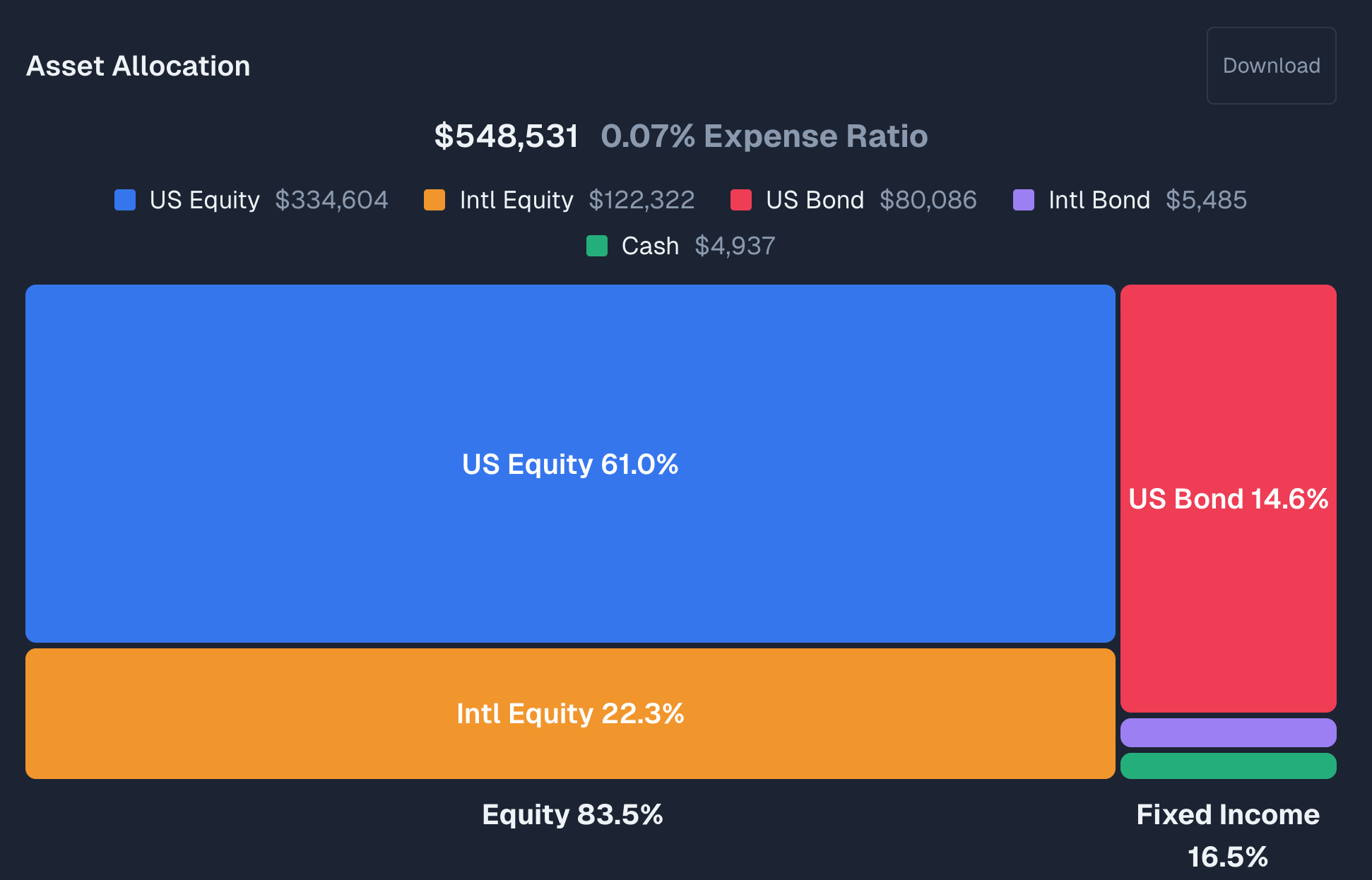

Retirement Planner

Full lifecycle optimizer — savings waterfall, Roth conversions, Social Security, withdrawal sequencing.

Tax FilingTax Refund Estimator

Federal + state refund or amount owed with full bracket calculation.

TaxTax Brackets

See which 2026 brackets your income falls in. Marginal and effective rates.

Retirement401(k) Optimizer

Roth vs. Traditional, employer match, tax savings at every contribution level.

RetirementRoth Conversion

Tax cost today vs. tax-free growth. Includes IRMAA and state taxes.

InvestmentsCapital Gains Tax

NIIT, bracket stacking, qualified dividends, and state taxes on investment gains.

Two questions. Both answered.

The advisory industry survives on self-serving obfuscation and archaic compensation systems. We provide unbiased, conflict-free clarity, free to all.

Where is my money going?

Financial statements that balance to the penny. Income, spending, taxes, and investment returns — decomposed, categorized, and reconciled. Not an approximation. The actual answer.

What should I do?

Tax-optimized savings. Roth conversion strategy. Social Security claiming ages. Withdrawal sequencing. The interactions are too complex to solve by hand. The engine solves them in 2 seconds.

Every page teaches something

This isn’t a dashboard. It’s a curriculum. Each page exists because it changed how someone thinks about their money.

Your real marginal rate swings from negative 60% to >100%

The tax code is infinitely complex and hardly anyone understands how it truly works. Federal brackets, FICA, state taxes, EITC, ACA subsidies, IRMAA cliffs, the SS torpedo — they all stack. I built the most sophisticated personal tax engine that exists, covering all 50 states. It’s free. No login, no paywall.

See your real rate

See your real rateSmall fees can destroy 50%+ of your future wealth

Your brain has no intuition for how destructive a “small” 1–2%/yr fee is over a lifetime. High-fee funds and advisor AUM fees quietly transfer your wealth into their accounts. It’s not an accident that fund managers and financial advisors are so well off — they collect their management fees regardless of how your investments perform.

“Do not allow the tyranny of compounding costs to overwhelm the magic of compounding returns.” — John Bogle, Vanguard founder and index fund pioneer

You earned it. Where did it all go?

Every dollar you earned, decomposed into taxes, living expenses, and what you actually kept. Year by year. The answer is usually humbling — and motivating.

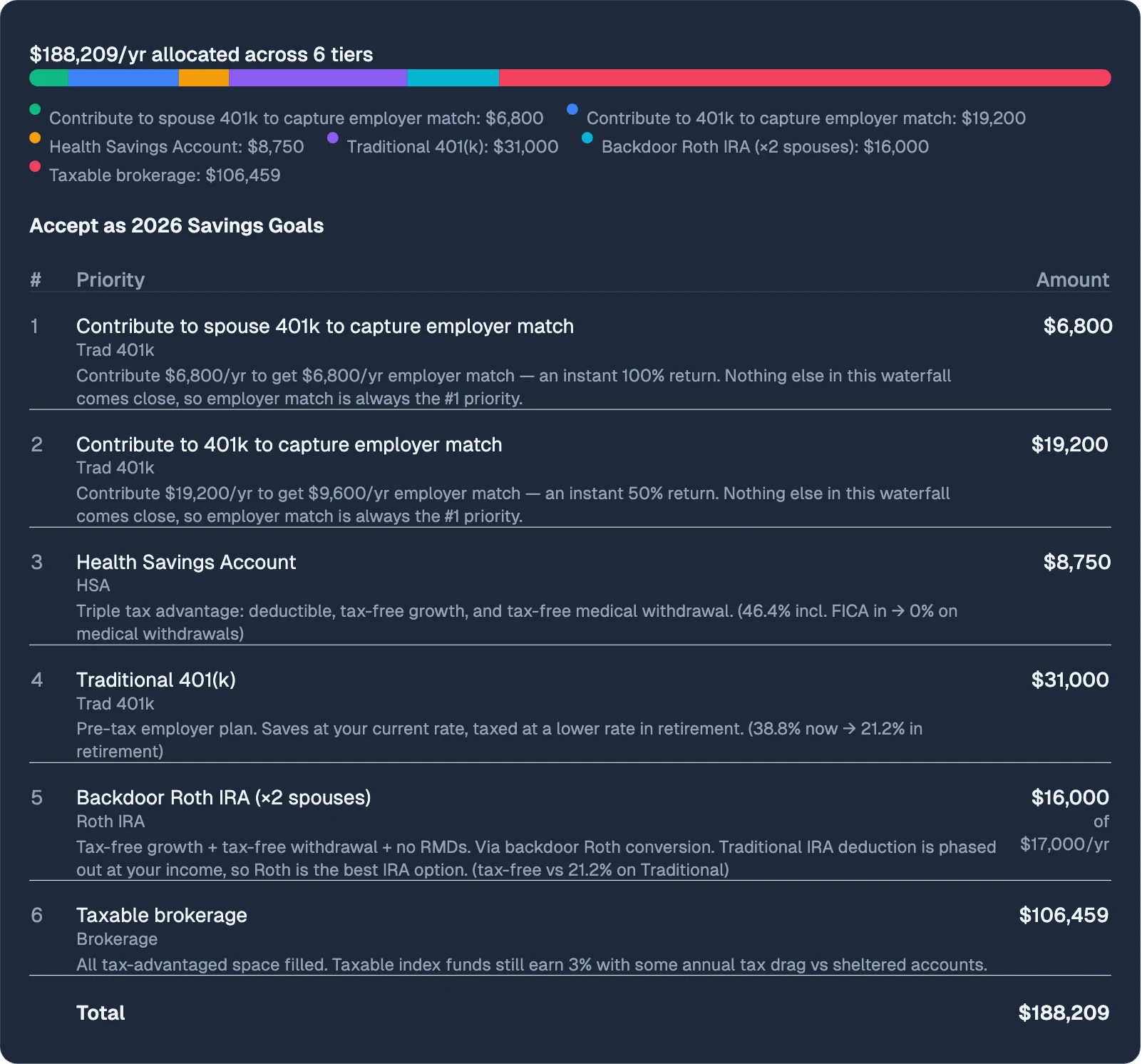

Stop guessing which accounts to fund first

401k to maximize employer match, HSA, Roth or Traditional, mega backdoor, taxable — the optimal order depends on your marginal rate, employer match, and timeline. The engine computes your personal waterfall.

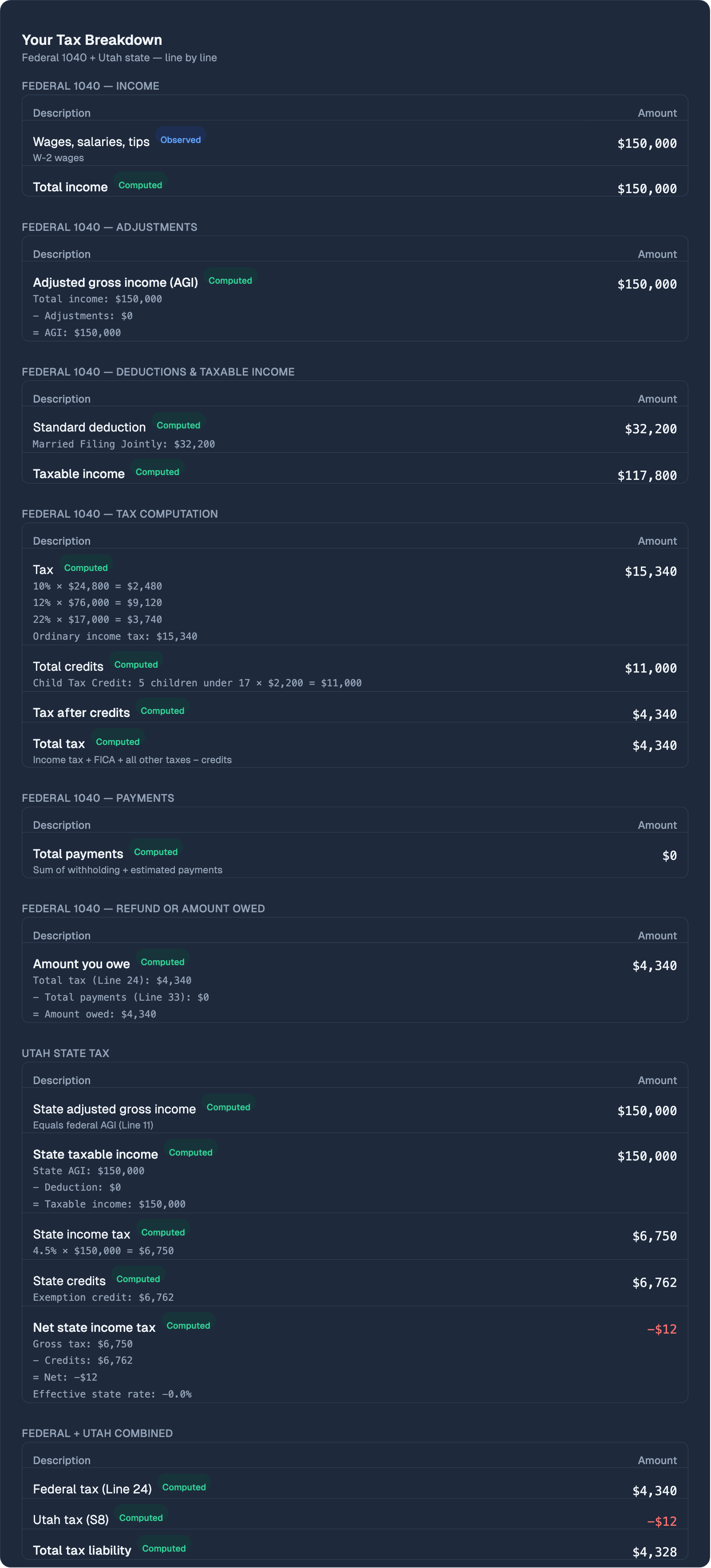

Your full 1040, computed line by line

Federal income, adjustments, deductions, tax computation, payments, refund or amount owed — plus your state return. Every line sourced, every number explained.

I wanted to be a financial advisor — I couldn’t stomach the compensation model.

I shadowed financial advisors in my early 20s. Nice cars, beach condos in Maui, visibly happy. But the lifestyle is built on an inconvenient truth — the industry is self-serving.

One advisor I shadowed targeted recently retired public school teachers. Why retirees? Because 1% of a 60-year-old’s portfolio pays far more than 1% of a 25-year-old’s — and advisors can’t touch your 401k until you roll it over to them after leaving your employer.

I couldn’t justify extracting wealth from the people I was trying to help. I knew the debilitating math of compounded fees. So I became a finance PhD instead, and built software that gives the same advice — the planning engine is free, and account aggregation, statements, charts, and spending analysis are $49.99/yr — or $99.99/yr for your whole family. Free for the first 18 months.

The math is genuinely hard. Roth vs. Traditional depends on your marginal rate across multiple tax systems. Social Security claiming depends on your withdrawal strategy, which depends on your Roth conversion plan. It’s circular. You need the most sophisticated optimizer ever built for this problem. So I built one — and I’m giving it away for free.

You now have better tools than any financial advisor on the planet.

How we compare

Deeper than anything at any price point.

| Feature | Budgeting Apps* | AUM Advisors** | Torv Free | Torv from $49.99/yr |

|---|---|---|---|---|

| No conflicts of interest† | ✓ | ✗ | ✓ | ✓ |

| Unbiased savings & withdrawal sequencing | ✗ | ✗ | ✓ | ✓ |

| Roth conversion strategy | ✗ | ? | ✓ | ✓ |

| Tax trap detection (IRMAA, ACA, SS torpedo) | ✗ | ? | ✓ | ✓ |

| Social Security optimization | ✗ | ? | ✓ | ✓ |

| 1040 tax breakdown (federal + state, line by line) | ✗ | ✗ | ✓ | ✓ |

| Enterprise-grade financial statements | ✗ | ✗ | ✗ | ✓ |

| Bank & investment account syncing | ✓ | ✗ | ✗ | ✓ |

| Automatic transaction categorization | ✓ | ✗ | ✗ | ✓ |

| Spending analysis + trends | ✓ | ✗ | ✗ | ✓ |

| Cash flow forecasting | ✗ | ✗ | ✗ | ✓ |

| Compensation model | ~$100/yr | 1%/yr for life | free | $49.99/yr |

| Annual fees as your portfolio grows | ||||

| $100K portfolio | ~$100/yr | $1,000/yr | free | $49.99/yr |

| $1M portfolio | ~$100/yr | $10,000/yr | free | $49.99/yr |

| $10M portfolio | ~$100/yr | $100,000/yr | free | $49.99/yr |

| Annual retirement budget, saving $X/year from age 25–60*** | ||||

| Saving $25K/yr | $50K/yr49% lost | $50K/yr49% lost | $99K/yr | $99K/yr |

| Saving $50K/yr | $100K/yr49% lost | $100K/yr49% lost | $197K/yr | $197K/yr |

| Saving $75K/yr | $150K/yr49% lost | $150K/yr49% lost | $296K/yr | $296K/yr |

| Saving $100K/yr | $200K/yr49% lost | $200K/yr49% lost | $395K/yr | $395K/yr |

| Earliest retirement age to produce $100K/year of income, saving $X/year starting at age 25*** | ||||

| Saving $25K/yr | age 7211 years later | age 7211 years later | age 61 | age 61 |

| Saving $50K/yr | age 6010 years later | age 6010 years later | age 50 | age 50 |

| Saving $75K/yr | age 549 years later | age 549 years later | age 45 | age 45 |

| Saving $100K/yr | age 497 years later | age 497 years later | age 42 | age 42 |

Show footnotes

* Budgeting Apps includes Monarch Money, YNAB, Copilot Money, and similar personal finance trackers. They excel at spending tracking and categorization but offer no retirement planning, tax optimization, or withdrawal strategy capabilities.

** This column reflects a typical AUM (assets under management) advisor — the industry default. Fee-only fiduciary advisors who charge flat hourly or project rates are a different breed entirely and can be excellent. The problem is ~90% of the industry is AUM-based, and you often can’t tell what you’re getting until years later — after the fees have compounded.

AUM 2% drag: 1% AUM fee, 0.5% excess fund expense ratios (actively managed vs. index), 0.3% tax drag from portfolio churning, 0.2% from tax-inefficient account placement. A typical conflicted advisor, not worst-case. “Unbiased” savings/withdrawal sequencing: AUM advisors have a financial incentive to discourage tax-advantaged accounts (401k, IRA, HSA) that reduce assets under their management.

† Common AUM advisor conflicts of interest: discourage tax-advantaged accounts (401k, IRA, HSA) that reduce assets under management; recommend actively managed funds with higher expense ratios; discourage paying off mortgage or debt to keep assets higher; churn portfolios to justify fees; avoid Roth conversions that shift assets out of taxable accounts; and introduce unnecessary portfolio complexity (and thus tax headaches) to give the appearance of adding value.

*** Projection assumptions: start saving at age 25, 4% real return (after inflation), 2% drag reduces real return to 2%, portfolio depleted to $0 at age 95. All amounts in real (inflation-adjusted) dollars. The math: when accumulation and drawdown periods are equal, annual spending = annual savings × (1+r)n. At 4% for 35 years that’s 3.95×; at 2% it’s exactly 2×.

Questions the engine answers

“Should I do Roth or Traditional?”

It depends on your tax rate now vs. later. Most tools get this wrong because they don’t compute your actual marginal rate across all brackets, FICA, state taxes, and phase-outs. The engine does.

“When should I claim Social Security?”

It’s not just about break-even age. It interacts with your withdrawal strategy, tax brackets, IRMAA surcharges, and your spouse’s survivor benefit. The optimizer evaluates all of it simultaneously.

“Am I saving enough? In the right accounts?”

Rules of thumb like “save 15%” ignore your tax situation, existing balances, employer match, and timeline. The engine computes exactly how much, in which accounts, in what order. See your waterfall.

“Do I even need a financial advisor?”

You should know what the math says before you pay someone 1% of your wealth every year. Over 30 years, that 1% quietly erodes 25–50% of what you could have had. See the numbers yourself — for free — and then decide.

Every calculator is free. No login required.

Free book: A Book about Wealth

The blueprint behind the app. Six levers that determine your lifetime wealth — starting capital, earnings, taxes, spending, investment returns, and interest expense. Written for recent grads and anyone who wants to understand how money actually works.

60 pages. No fluff. No upsell. The book teaches the framework; the app computes it.

Download free (PDF)Your data is encrypted. Here’s the proof.

Most financial apps say “bank-level encryption” and show a lock icon. Here’s what our database actually stores.

| user_id | account_name | institution | balance |

|---|---|---|---|

| a1b2c3d4e5...7d6c | enc:3a7f1b:c9e2d4:8b1f... | enc:7d4e2a:f1b3c5:2e9a... | $47,832.19 |

| a1b2c3d4e5...7d6c | enc:5c8d2e:a4f1b7:6d3e... | enc:9b2f4a:d7e3c1:4a8f... | $312,457.83 |

Simple, honest pricing

Every tool is free. No login required. Pay when you want your data saved and accounts synced.

We think once you see your full financial picture, you won't want to go back.

- Tax calculator (50 states + DC)

- Retirement savings & withdrawal optimizer

- Social Security claiming strategy

- Where to save next (401k → IRA → HSA → taxable)

- Financial projection over entire life

- Roth conversion, IRMAA, RMD, capital gains

- 11 calculators, all free

- Link your accounts — banks, brokerages, loans

- Income statement, balance sheet, cash flow — to the penny

- Categorize once, automated forever

- Every hidden investment fee, exposed

- Net worth history across all accounts

- Cash flow — where it went, where it's going

- Up to 5 people (you + 4 family)

- Fully independent accounts — no shared data, no visibility between members

- Each person gets their own statements, categorization, and projections

- As low as $20/person/yr

If the sponsoring subscriber cancels, family members get 30 days to convert to their own plan or drop to the free tier.

Ready to see your numbers?

Every tool is free. No login required. Sign up when you want your data saved and accounts synced.